Restrictions on Prepayment

So you have a commercial real estate loan and want to refinance because rates are low? Unfortunately, almost all non-recourse loans involve restrictions on prepayment. Restrictions on prepayment are intended to preserve the lender’s yield on your loan and to guarantee a certain amount of profit. These restrictions will impede business flexibility if you need to quickly refinance or sell the asset.

When a lender originates a mortgage, the interest and payments are calculated based on a certain maturity. Lenders expect to receive a certain amount of interest on each mortgage they underwrite according to those parameters. For that reason, prepayment penalties are often imposed on borrowers. The lender would do a risk calculation or a yield calculation, and the penalty itself was generally set between 2 percent and 4 percent of the loan.

Prepayment penalties are used as a way to entice buyers with low rates while locking in lenders’ returns. In commercial lending, this is termed the defeasance fee and is the amount needed for the loan manager to take the profits of the borrower’s payoff, plus the prepayment penalty, and go out in the marketplace to buy an asset with the same yield and the same maturity.

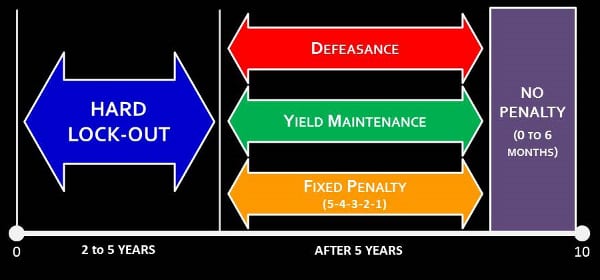

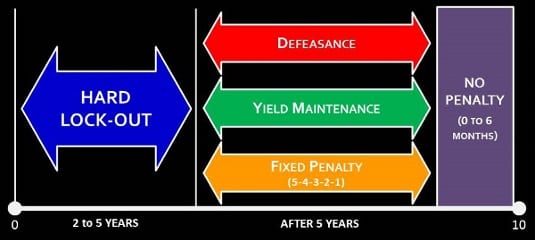

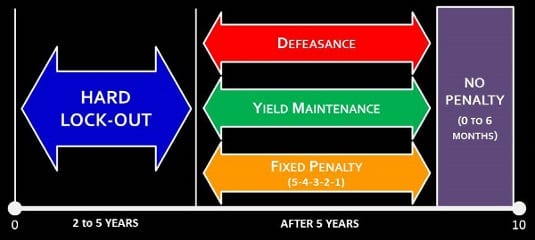

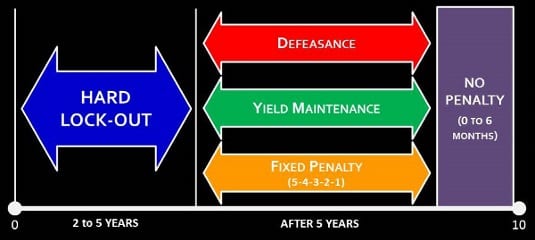

Generally, the lender will now allow the borrower to pay back the loan during the first 2 to 5 years. After the lock-out period, the loan can be prepaid but usually at a severe cost to the borrower. As the loan continues to mature, prepayment penalties decrease in severity. The longer you’ve had your loan and the less you owe, the smaller your penalty will be. So restrictions on prepayment involve three common penalties. See the visual summary then checkout the descriptions below.

Restrictions on Prepayment: A Visual Summary

Defeasance

Defeasance requires the borrower purchase a set of US Treasury securities whose coupon payments exactly replicate the cash flows the lender will lose as a result of the prepayment. Instead of paying cash to the creditor, the defeasance option allows the debtor to exchange another cash flowing asset for the original collateral for the loan. This asset exchange allows creditors to continue to obtain their expected profit throughout the loan term without having to find new lending opportunities to change the prepaid capital.

Yield Maintenance

Yield Maintenance (YM) requires the borrower pay the remaining principal and the present value (as defined by the note) of the remaining interest. It is intended to make investors uninterested to prepayment. It also makes refinancing unappealing and uneconomical to debtors. The formula for yield maintenance is, YM = Present Value of Remaining Payments x (Bond Interest Rate – Rate on a Treasury Note). Note that the Treasury rate should be for bonds of the same duration as the mortgage in question.

Fixed Penalty

A fixed penalty is a fixed percentage of the remaining balance of the loan. For example, it could be 5 percent in year one, 4 in year two, 3 percent in year three, etc. This penalty often depreciates as the number of payments remaining reduces and may eventually burn off. Calculating the penalty is as simple as taking your most recent mortgage statement and multiplying the outstanding debt by the current penalty amount. This total will simply be added to your payoff statement at closing.

Helpful Resources for Restrictions on Prepayment:

Shelton Business Services…BairdHolm…UMKC…Real Estate Research Institute…Financial Dictionary

Pingback: jpr

Pingback: udp

Pingback: albp

Pingback: Fort Lee

Pingback: jpdhr

Pingback: acupuncture

Pingback: udaipur

Pingback: manali call girl

Pingback: mumbai call girl

Pingback: dehradun call girl

Pingback: blog escorts

Pingback: bangalore escorts

Pingback: health blog

Pingback: health world

Pingback: crypto news

Pingback: richest vietnamese houston

Pingback: nepo hat

Pingback: jadore cowboy

Pingback: need money for porsche

Pingback: brazil crop top

Pingback: swimsuits houston texas

Pingback: french bulldog accessories

Pingback: frenchie chihuahua mix

Pingback: frenchie chihuahua mix

Pingback: frenchie boston terrier mix

Pingback: frenchie boston terrier mix

Pingback: floodle puppies for sale

Pingback: frenchie chihuahua mix

Pingback: fart coin

Pingback: folding hand fans

Pingback: blue color french bulldog

Pingback: lilac french bulldogs

Pingback: fluffy french bulldog

Pingback: merle french bulldog

Pingback: french bulldogs

Pingback: french bulldogs

Pingback: floodle

Pingback: crypto news

Pingback: surrogacy mexico

Pingback: french bulldog puppies for sale houston

Pingback: travel buddy

Pingback: micro bully

Pingback: probiotic dog treats

Pingback: french bulldog puppies texas

Pingback: clima queretaro

Pingback: linh hoang houston

Pingback: in vitro fertilization mexico

Pingback: in vitro fertilization mexico

Pingback: in vitro fertilization mexico

Pingback: in vitro fertilization mexico

Pingback: best food for bernedoodles

Pingback: in vitro fertilization mexico

Pingback: how to obtain dog papers

Pingback: clima de veracruz

Pingback: playnet

Pingback: linh hoang

Pingback: cover band los angeles

Pingback: french bulldog puppies near me for sale

Pingback: french bulldog puppies for sale $200

Pingback: blue french bulldog

Pingback: French Bulldog puppies in Austin

Pingback: bitcoin

Pingback: collab

Pingback: French Bulldog Texas

Pingback: french bulldog rescue

Pingback: linh hoang houston

Pingback: best joint supplement for dogs

Pingback: crypto

Pingback: canine probiotics

Pingback: dogs papers

Pingback: mem

Pingback: how can you get papers on a dog

Pingback: french bulldog

Pingback: how to obtain dog papers

Pingback: how to obtain dog papers

Pingback: how to get papers for a dog

Pingback: blue french bulldog

Pingback: joyce echols

Pingback: what is a cavapoo dog breed

Pingback: what is a maltipoo dog

Pingback: miniature bulldog

Pingback: saint berdoodle grooming

Pingback: dogs mustache

Pingback: aussiechon

Pingback: pomsky color

Pingback: ragnarok online server

Pingback: delhi cg

Pingback: MyBlog

Pingback: enclomiphene substitute over the counter

Pingback: sans ordonnance kamagra sans prescrire pilule contraceptive

Pingback: androxal no perscription usa fedex shipping

Pingback: how to order dutasteride cheap in canada

Pingback: levitra benefits over flexeril cyclobenzaprine

Pingback: discount online gabapentin

Pingback: discount fildena purchase tablets

Pingback: buy itraconazole canada discount

Pingback: lowest price generic avodart

Pingback: ordering rifaximin australia suppliers

Pingback: comprar xifaxan en natural sex

Pingback: pouze doručení kamagra

Pingback: wix seo experts

Pingback: wix seo experts

Pingback: wix seo service

Pingback: wix seo specialists

Pingback: wix seo experts

Pingback: video chat

Pingback: cam sex

Pingback: free sex cams

Pingback: free webcam sex

Pingback: cheap sex webcams

Pingback: cheap adult webcams

Pingback: cheap sex chat

Pingback: cheap sex webcams

Pingback: live sex webcams

Pingback: live amateur webcams

Pingback: cheap sex cams

Pingback: cheap sex shows

Pingback: live sex webcams

Pingback: webcam girls

Pingback: live webcam girls

Pingback: live sex webcams

Pingback: rebirthro

Pingback: casino en ligne le plus payant

Pingback: time zone meeting planner

Pingback: time between two times

Pingback: namaz time today

Pingback: utc clock

Pingback: cron schedule calculator

Pingback: time zone converter

Pingback: office working days calculator

Pingback: daily sunrise time

Pingback: epoch converter

Pingback: duncg

Pingback: trx address generator

Pingback: trc20 scan

Pingback: crypto vanity address

Pingback: tron address scan

Pingback: trc20 generator

Pingback: free webcam sex

Pingback: live cam girls

Pingback: free adult webcams

Pingback: virtual mailbox service

Pingback: registered agent software

Pingback: CA New Constructions Homes

Pingback: Bay Area San Jose Best Realtor

Pingback: Silicon Valley CA Fixer Upper Home Search

Pingback: kooky

Pingback: cyclosporine immunoassay